It usually shows up at the worst possible moment. The car needs a repair nobody saw coming, a hospital hands you a bill, or a cousin’s wedding quietly costs twice what anyone admitted up front. The money has to come from somewhere — and for most of us in India, that somewhere is either a credit card or a personal loan.

So, which do you reach for?

That one decision, usually made in a hurry, drains thousands of rupees from borrowers every year. Both options put cash in your hands fast. The catch is that they’re wired very differently underneath, and picking the wrong one can stretch a one-off expense into months of avoidable interest.

We’ve spent the better part of a decade at Loanedz watching people wrestle with this exact question. What follows is the plain-English version of what we tell them — no jargon, no hard sell, just the stuff that actually helps you choose.

Why This Loan Comparison Matters More Than Ever in 2026

Borrowing in India has become almost too easy. Approvals land in minutes, the cash hits your account before lunch, and your credit card will happily turn any purchase into an EMI with a single tap. Convenient? No argument there. But that smoothness has a way of hiding what the money really costs you.

Here’s what most people miss. The gap between a interest rate and credit card loan charges can run north of 30 percentage points a year. On a ₹3 lakh borrowing, that’s the difference between paying back roughly ₹3.5 lakh and handing over ₹4.2 lakh or more for the very same money.

None of this is about one option being virtuous and the other being a trap. A good loan comparison is really just about fit — matching the right tool to your particular situation. Let’s get into the nuts and bolts.

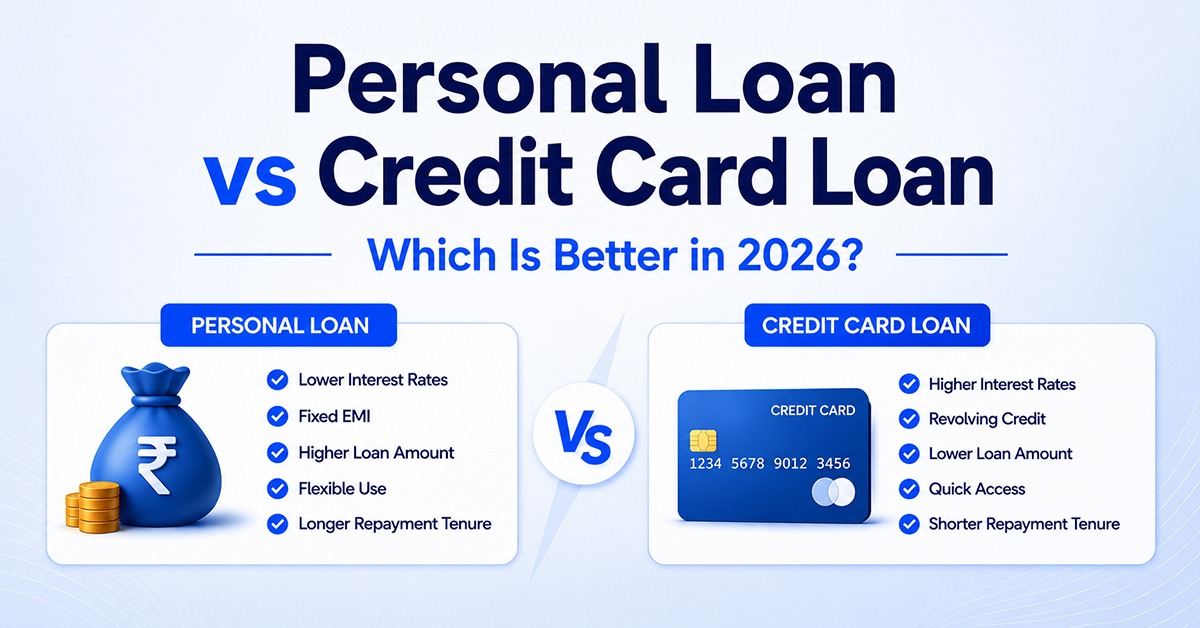

What Is a Personal Loan?

A Personal Loan is money a bank or NBFC lends you without asking for security — no property, no gold, nothing pledged. You borrow a fixed amount, agree on a fixed tenure, and in most cases lock in a fixed interest rate.

The full sum lands in your account at once, and you repay it in equal monthly EMIs, usually over one to five years. Some lenders will stretch that to seven or eight.

The quiet advantage here is certainty. Your rate and your timeline are set on day one, so you know your EMI down to the rupee. Nothing creeps up on you later.

Key Features of a Personal Loan

No collateral. Approval rides on your income, your credit score, and where you work.

Fixed EMIs, which makes planning the month genuinely easier.

Lower rates. As of mid-2026, personal loans start near 8.75% a year at public sector banks like Union Bank of India and Bank of Maharashtra, and around 9.99% at private players such as HDFC, ICICI, and Axis. NBFCs sit higher — roughly 14% to 24% — depending on who you are on paper.

Bigger amounts, anywhere from ₹50,000 to well past ₹40 lakh.

A processing fee, usually 1% to 3% of the loan, with 18% GST on top.

This is the option that fits planned, sizeable spending — a home renovation, a wedding, tuition, consolidating other debt, or a medical bill you need a little breathing room to clear.

What Is a Credit Card Loan?

“Credit card loan” is really a catch-all phrase for a few different ways of borrowing against your card:

Revolving credit — what happens when you don’t clear your full bill and let the balance roll over.

Loan on credit card — a pre-approved amount handed to you against (or sometimes beyond) your card limit.

EMI conversion — chopping a big purchase or an outstanding balance into monthly instalments.

What makes a card tempting is sheer convenience. Clear your statement in full by the due date and you get an interest-free window of up to 45 to 50 days. Used that way, it’s essentially a free short-term loan — and honestly, that’s the smartest way to use one.

Key Features of a Credit Card Loan

Instant access to credit you already have, with no fresh paperwork.

An interest-free stretch, as long as you pay the bill in full and on time.

Steep interest the moment you don’t. Revolving balances in India typically run 2.5% to 3.5% a month — which compounds into a painful 30% to 45% a year.

EMI conversion softens that, but it still usually costs more than a personal loan.

Add-ons that pile up: conversion fees, late payment charges (often ₹500 to ₹1,500), and GST.

A card earns its keep for small, short-term needs you’re confident you can clear quickly. Push it past that and the math turns against you fast.

Personal Loan vs Credit Card Loan: The Side-by-Side Comparison

If you just want the quick scan, here’s how the two stack up:

Personal Loan Interest Rate vs Credit Card Loan Charges in 2026

This is the part that decides whether you come out ahead or behind.

A personal loan interest rate works on a reducing balance. Translation: you’re only charged interest on what you still owe, and since that shrinks every month, so does the interest. Pair that with rates under 10% at the better banks and the total cost stays firmly in check.

Credit card loan charges behave differently — and not in your favor. Three percent a month sounds almost trivial until you let it compound across a year and watch it sail past 40%. Add late fees and GST, and a balance that looked manageable starts to balloon. The real wallet-killer is paying just the “minimum due,” usually around 5% of what you owe. Do that long enough and you can end up repaying two or three times what you originally spent. We’ve seen it happen plenty of times, and it’s never pretty.

The short version: if you can’t wipe it out inside the interest-free window, a personal loan is almost always the cheaper way to borrow.

A Real-World Example: ₹3 Lakh, Two Very Different Bills

Numbers land harder than any explanation. Say you need ₹3,00,000 and plan to clear it over two years.

Personal loan at 11% a year: your EMI sits around ₹13,978. Total interest across 24 months works out to roughly ₹35,475 — so you repay about ₹3,35,475.

The same ₹3 lakh riding as a credit card balance at ~36% a year (that’s the 3%-a-month figure): the interest alone could cross ₹1,20,000 over the same stretch. More than three times the loan.

(These are illustrative figures — your actual rate depends on your credit score, income, and lender.)

Same money, same two years, wildly different outcome. For anything large that you’ll repay over months, the loan quietly saves you a small fortune.

When Should You Choose a Personal Loan?

A personal loan is usually the right call when:

You need a meaningful sum — typically north of ₹50,000.

You want a longer, predictable runway with fixed EMIs.

You’re consolidating debt, including clearing an expensive card balance.

You’re funding something planned: a wedding, a renovation, education, a medical procedure.

You care most about keeping the total interest as low as possible.

When Does a Credit Card Loan Make Sense?

A card can genuinely be the smarter pick when:

You need a small amount in a hurry and can clear it within 30 to 50 days.

You’ll pay the full bill on time and walk away owing zero interest.

You’ve got a real 0% EMI offer with no processing fee hiding in the fine print.

You’d rather skip the hassle of a fresh loan application.

The one rule worth tattooing on your brain: only put on your card what you can pay back fast.

Your Loan Decision Guide: 5 Questions to Ask Before You Borrow

Before you commit to either, sit with these five questions. They’re the same ones we’d walk you through over a call:

How much do I actually need? Small and short-term leans toward the card; large and drawn-out leans toward a loan.

Can I clear it inside the interest-free window? If yes, the card can cost you nothing. If no, compare rates properly.

What’s my real rate — and is it on a reducing balance? Look at the annual figure, not the friendly-looking monthly one.

What else am I being charged? Processing fees, GST, late fees, prepayment penalties — they add up.

Will my EMI stay under 40% of my take-home pay? Keeping all your EMIs below 40–50% of income is what keeps you sleeping at night.

Common Mistakes Borrowers Make (And How to Avoid Them)

A few traps we see again and again:

Paying only the minimum due. It feels responsible. It isn’t — it quietly multiplies what you owe. Pay in full or move the balance to a personal loan.

Fixating on the headline rate. A “low” rate with a 3% fee can cost more than a slightly higher rate with none.

Skipping the comparison. Even a 1% difference in your personal loan interest rate is real money over a few years.

Applying everywhere at once. Each hard enquiry chips at your credit score. Compare first, apply once.

Borrowing more than you need. Every extra rupee comes with interest attached.

The Verdict: Which Borrowing Option Wins in 2026?

There’s no trophy winner here — only the option that fits your situation.

If it’s a small, short-term need you can clear inside the interest-free period, a credit card is convenient and can even cost nothing. If it’s a larger amount, a longer timeline, or debt you’re trying to consolidate, a personal loan wins on cost, predictability, and plain peace of mind nearly every time.

For most real borrowing situations in 2026, the lower rates and fixed EMIs of a personal loan make it the more sensible choice. But don’t take that as gospel — run your own numbers, because yours is the only situation that counts.

Still on the fence?

That’s exactly what we’re here for. Loanedz pairs over ten years in financial services with technology that compares personal loans across leading banks and NBFCs — so you land the right one, at the right rate, without drowning in paperwork.

Compare your personalized loan options with Loanedz today. Quick, transparent, and built around your numbers — not someone else’s. Start here

Frequently Asked Questions

Is a personal loan cheaper than a credit card loan?

Usually, yes. In 2026, bank personal loans start somewhere around 8.75%–9.99% a year, while a rolled-over credit card balance can cost 30%–45%. For anything sizeable that you’ll repay over several months, the personal loan is the cheaper borrowing option more often than not.

What is the interest rate on a credit card loan in 2026?

Revolving credit typically runs 2.5%–3.5% a month, which works out to roughly 30%–45% a year. Converting to EMI brings that down, but it still tends to sit above a personal loan.

Can I convert my credit card balance into EMIs?

Yes — most banks and card issuers let you turn an outstanding balance or a big purchase into monthly instalments. It’s easier on your cash flow and cheaper than letting the balance revolve, though the rate is usually still higher than a personal loan.

Does a credit card loan affect my credit score?

It can go either way. High utilization and missed payments drag your score down. Borrow sensibly and repay on time, and it can sit neutral or even work in your favor.

When should I pick a credit card loan over a personal loan?

When the amount is small and you can clear it inside that 45–50 days interest-free window, or when there’s a genuine 0% EMI offer with no hidden fees. For anything bigger or longer, a personal loan is the better bet.

How do I get the lowest personal loan interest rate?

Keep your credit score above 750, hold down a steady job and income, compare a few lenders before you commit, and don’t be shy about negotiating the processing fee. If you already bank somewhere, ask about pre-approved offers — they’re often cheaper.