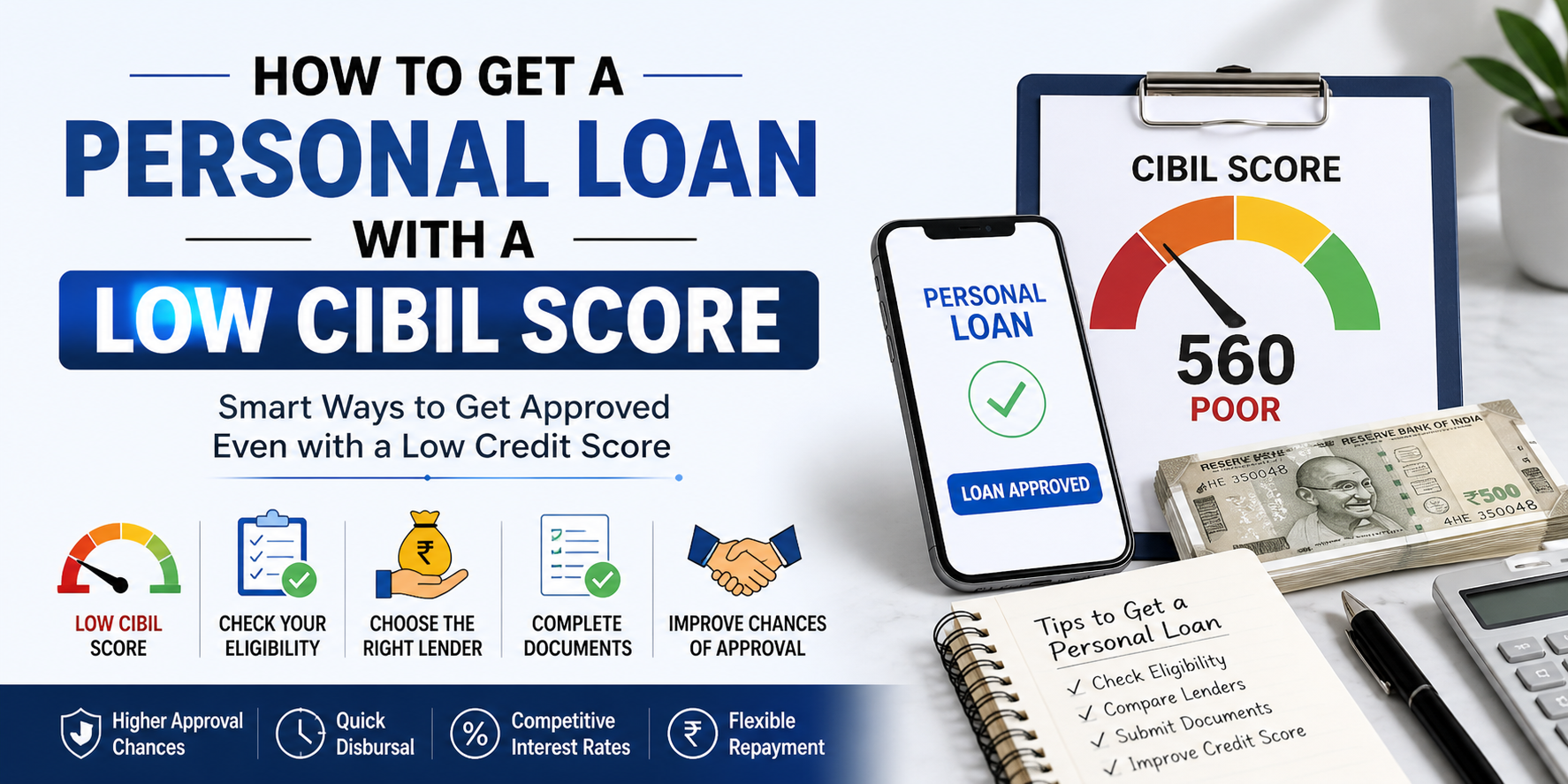

The rejection letter from a bank is a heavy blow. Usually, it comes right when you need funds the most - perhaps for a sudden medical emergency, an urgent home repair, or a bridge between paychecks. More often than not, that "No" is driven by a single three-digit number: your CIBIL score.

The reality of lending in India has shifted. While traditional banks still prefer the "safe" 750+ score, the rise of NBFCs and fintech platforms has opened doors that were previously locked. A low score makes the process harder, but it certainly doesn't make it impossible.

This blog post cuts through the jargon to show you exactly how to secure a loan when your credit history isn't perfect. If your credit isn't great, you can still find lenders and compare real offers that fit your situation on Loanedz. It’s harder than having a perfect score, but it’s far from impossible.

What Defines a "Low" CIBIL Score Today?

In India, CIBIL scores range from 300 to 900. While a score of 750 is the gold standard for low-interest rates, lenders today are more nuanced in how they view "risk."

How Can You Get Approved With Poor Credit?

If you are currently sitting in the 600-650 range, you need a strategy that proves your "ability to pay" outweighs your "past mistakes." Here is how to do it:

Apply with NBFCs and Fintech Lenders: Private banks have rigid algorithms. NBFCs (Non-Banking Financial Companies) like Tata Capital or Bajaj Finserv, and fintech apps like Fibe or KreditBee, use "alternate data." They look at your monthly salary, spending habits, and professional stability rather than just your CIBIL report.

Add a Co-Applicant or Guarantor: This is the fastest way to bypass a low score. If a family member with a 750+ score joins your application, the lender takes on their credit profile as a safety net. This often results in lower interest rates as well.

Provide Solid Proof of Income: A low score suggests past trouble, but a high current salary suggests a bright future. Show your last six months of bank statements, latest Form 16, and salary slips. If your income has recently increased, make that the centerpiece of your application.

Opt for a Lower Loan Amount: Asking for ₹10 Lakhs with a 610 score is a recipe for rejection. Start small. A ₹50,000 or ₹1 Lakh loan is easier to approve and serves as a "stepping stone" to rebuild your credit.

Fix Errors on Your Report: Sometimes your score is low because of a mistake - a loan you already closed that still shows as "active." Regularly checking your report for these discrepancies and raising a dispute with CIBIL can jump your score by 50+ points in weeks.

How Do You Secure Lower Interest Rates?

Every time a lender checks your credit, your score drops slightly (a "hard inquiry"). However, modern scoring models are smarter than they used to be.

If you apply to three different lenders within a 14 to 30-day window, these are often grouped as a single inquiry because the system recognizes you are "shopping" for one loan, not trying to take out three. Space your applications close together to protect your score.

How to Lower Your Interest Rate Even with Bad Credit

When you have a low score, you will likely be offered higher interest rates - sometimes between 18% and 28%. You can pull this number down by:

Maintaining a 30% Credit Utilization: If your credit card limit is ₹1 Lakh, try to never spend more than ₹30,000. Lenders see this and think you are responsible, not desperate.

Checking for RBI Compliance: Never borrow from an app that isn't a registered NBFC or tied to a bank. Check the RBI website to verify. Legitimate lenders are more likely to offer fair terms.

Longer Tenures: While this costs more in total interest, it lowers your Monthly Installment (EMI), making the lender feel more confident that you won't default.

How do you start your loan application on Loanedz today?

A low CIBIL score is a snapshot of the past, not a permanent label. By choosing the right lender and proving your current financial health, you can get the funds you need while simultaneously rebuilding your credit for the future.

If you want to stop guessing and see which lenders are actually a match for your current profile, you can check your eligibility on Loanedz. It takes less than a minute, performs a "soft check" that won't hurt your score, and shows you exactly where you stand in today's market.

Stop worrying about rejection. See which lenders want to work with you in 30 seconds. Check your Loanedz eligibility now!

FAQs

Can I get a personal loan with a CIBIL score of 600?

Yes. While major banks may decline, fintech lenders and smaller NBFCs frequently approve loans for scores around 600 if you have a stable job and a monthly salary above ₹25,000.

What is the minimum CIBIL score for a personal loan in India?

There is no universal minimum. Public sector banks usually require 720+, while fintech lenders may accept scores as low as 600. Below 600, you will likely need a co-applicant or collateral.

Will checking my own CIBIL score lower it?

No. Checking your own score is a "soft inquiry" and has zero impact on your credit rating. Only lender-initiated "hard inquiries" during a formal application affect your score.

How long does it take to fix a low CIBIL score?

Most borrowers see meaningful improvement within 3 to 6 months of consistent, on-time payments and reduced credit utilization. A full recovery typically takes 9 to 12 months.